Decentralized finance has changed how financial services handle money. Traditional banks funnel profits to shareholders—DeFi has to figure out how to pay everyone who keeps the system running: liquidity providers, token holders, developers, and treasuries. This matters if you’re evaluating yield opportunities, but it’s also just genuinely interesting if you want to understand how crypto economics actually work.

This guide covers where DeFi protocols make money and how they pass those earnings to participants.

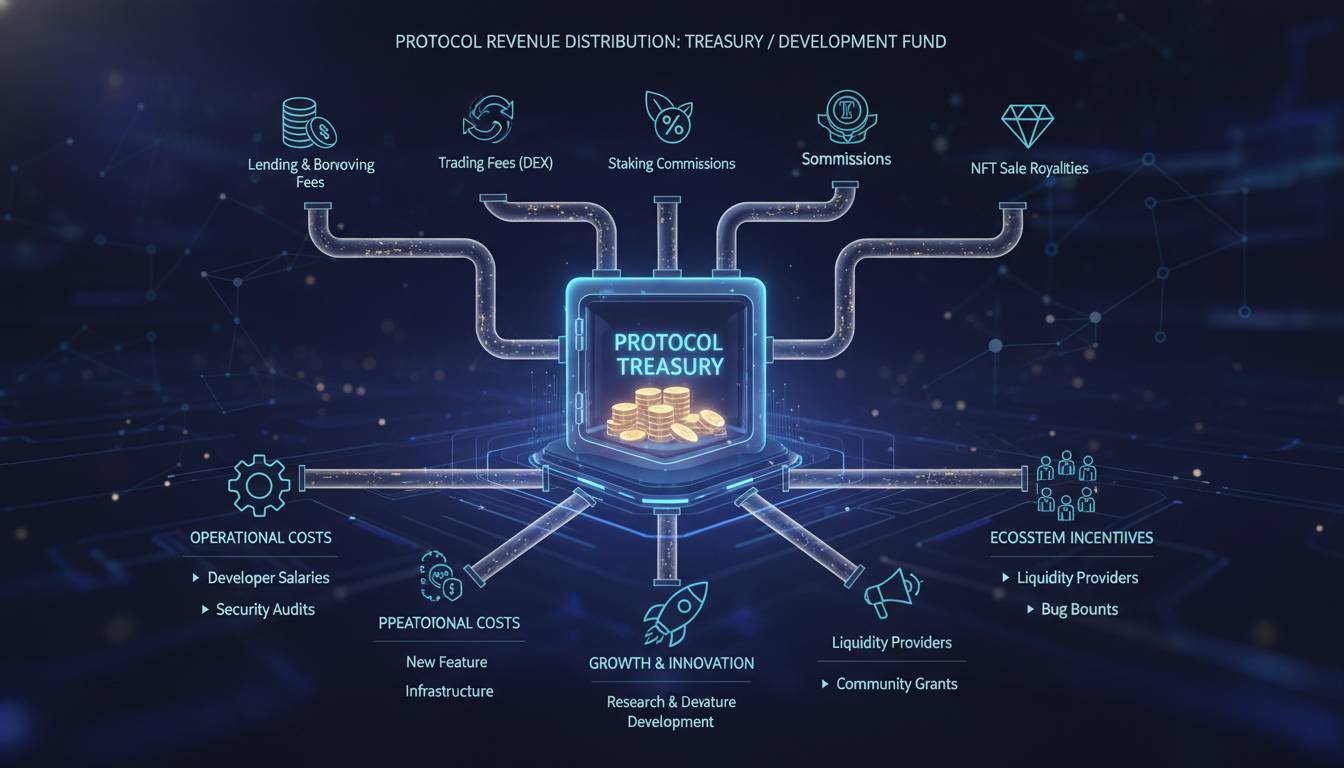

How DeFi Protocols Generate Revenue

First, you need to know where the money comes from. DeFi protocols generate revenue through several channels, each tied to a specific function.

Trading fees are the largest revenue source across most DeFi ecosystems. Decentralized exchanges like Uniswap and Curve charge a percentage of each swap—typically 0.3% for standard pairs on Uniswap V3. This fee goes to liquidity providers, but a portion often flows to the protocol treasury or gets burned as token buybacks, depending on the governance model.

Liquidity provider fees work differently. When you deposit assets into a liquidity pool, you earn a share of the trading fees generated by that pair. On Aave, borrowers pay interest, and a portion (around 10-20% depending on the asset and version) goes to the protocol as a flash loan fee or stays as reserves.

Interest spreads form the backbone of lending protocols like Aave and Compound. When users borrow assets, they pay an interest rate higher than what the protocol pays to depositors. The difference—the spread—generates revenue. Aave V3 introduced portal fees and adjusted how much flows to the protocol versus liquidity providers.

Staking rewards come from two sources: inflation (new tokens minted) and actual protocol revenue. Protocols like Lido and Rocket Pool generate fees from liquid staking derivatives, then distribute a portion to node operators while keeping the rest for the protocol.

Liquidation fees occur when collateral positions become undercollateralized and the protocol liquidates them. On MakerDAO, liquidations generate a stability fee plus a liquidation penalty, portions of which flow to the protocol.

Primary Revenue Distribution Models

Once revenue enters a protocol’s treasury or smart contracts, governance decides how it flows to participants. Four models dominate the space.

Staking Reward Distribution

The most straightforward model sends protocol revenue directly to token stakers. When you stake the native token, you receive a claim on future revenue proportional to your stake size and duration.

Uniswap’s fee switch exemplifies this approach. After years of governance debate, Uniswap V3 began directing a portion of trading fees to UNI stakers. The exact percentage varies by pool and has shifted over time as the community votes on parameters. Stakers lock their UNI tokens and receive weekly fee distributions in USDC or other stablecoins. The appeal is straightforward: you’re earning real yield rather than inflationary tokens.

The limitation is that staking rewards fluctuate based on trading volume. During market downturns, fee revenue can drop dramatically, leaving stakers with yields far below what they expected. There’s also impermanent loss—LP fees might not compensate for price movements in the underlying assets.

Treasury-Funded Grants

Many protocols accumulate revenue in a multisig treasury controlled by governance. These funds get allocated toward development grants, marketing, bug bounties, and ecosystem growth initiatives.

MakerDAO pioneered this model with its surplus buffer. When Dai borrowers pay stability fees, a portion fills the surplus buffer. Governance then votes on how to allocate these funds—often toward strategic reserves, development grants, or buybacks of MKR tokens (which are then burned to reduce supply).

The risk with treasury models is governance capture. If a small group of token holders controls the treasury, they may allocate funds toward their own interests rather than protocol growth. Transparency varies significantly across protocols—some publish detailed monthly reports while others offer minimal visibility into treasury operations.

Token Buybacks

When protocols generate consistent revenue, they often use those funds to purchase their own tokens from the market, then either burn them (reducing total supply) or distribute them to stakeholders.

The economic logic is straightforward: buybacks increase the value of remaining tokens by reducing supply while demand stays constant. For investors, this is preferable to receiving inflationary token rewards that dilute your holdings.

Curve DAO implemented a sophisticated version of this model. The protocol uses a “veTOKEN” system (explained in the next section) where revenue is distributed to voters who lock tokens for extended periods. When the protocol generates fees, it buys CRV from the market and distributes it to veCRV holders. The buyback pressure itself tends to support CRV’s market value.

The limitation is that buybacks only work when the token trades with sufficient liquidity. Thinly-traded tokens can see significant price impact from buyback programs, making the mechanism less effective than it appears on paper.

The veTOKEN Locking Model

Curve Finance introduced what became arguably the most influential revenue distribution mechanism in DeFi: the vote-escrowed token model.

Here’s how it works: users lock their governance tokens (CRV, in Curve’s case) for a period of one week to four years. In exchange, they receive “ve tokens” (veCRV) that represent their voting power and claim on protocol revenue. The longer you lock, the more ve tokens you receive.

The system aligns incentives well. Because ve tokens cannot be transferred or sold, locked users have a strong interest in protocol long-term health—they can’t simply dump their holdings if they disagree with a governance decision. Revenue flows to those who’ve demonstrated commitment through token lock-up, creating a self-reinforcing cycle of participation.

Several protocols have adopted variations of this model, including Balancer, Yearn Finance, and PENNY. The limitation is that it heavily favors large holders and long-term investors. Small participants may find the lock-up period too restrictive to participate meaningfully in revenue distribution.

Case Studies: How Top Protocols Distribute Revenue

Uniswap

Uniswap generates revenue through trading fees on V3 pools. Liquidity providers earn the majority of fees from their concentrated positions, but Uniswap Labs and the Uniswap DAO also capture a portion.

After governance approval, UNI token holders who stake their tokens receive a share of fee switch revenue. The exact allocation has evolved—early proposals debated whether fees should go entirely to stakers or split with liquidity providers. The current system favors stakers while ensuring LPs still earn competitive returns.

What’s notable is how Uniswap’s revenue distribution reflects its governance philosophy: slow, deliberate changes through community vote rather than top-down decisions.

Aave

Aave operates as a lending protocol where borrowers pay interest on loans, and depositors earn yield on supplied assets. The protocol retains a portion of the interest spread as revenue.

In Aave V3, the protocol introduced “portals” that allow bridges to route liquidity across networks. This generates portal fees that flow to the Aave DAO treasury. Governance controls how these funds get allocated—typically toward development, security audits, and ecosystem incentives.

Aave’s revenue model demonstrates how lending protocols can generate sustainable yield without relying on inflationary token rewards. The protocol has survived multiple market cycles, partly because its revenue model doesn’t require perpetually rising prices to function.

Curve

Curve’s revenue distribution is inseparable from its veTOKEN model. The protocol generates fees from stablecoin swaps and crvUSD stablecoin liquidations. These fees buy CRV from the market, which then gets distributed to veCRV holders.

The twist is that veCRV holders also control governance—proposals that affect fee distribution or token economics require their approval. This creates alignment: those receiving revenue also decide how the system operates.

Curve’s model has been successful, maintaining strong CRV demand even during bear markets when other tokens collapsed. The limitation is that it creates significant voting power concentration among a relatively small group of large holders.

MakerDAO

MakerDAO generates revenue through stability fees on Dai loans, liquidation penalties, and increasingly, real-world asset yields through Spark (the protocol’s DSR and lending arm).

The system has evolved significantly. Early MakerDAO burned MKR tokens with surplus revenue, reducing supply and creating deflationary pressure. More recently, the protocol shifted toward building substantial reserves through its surplus buffer, which now exceeds several hundred million dollars in value.

MakerDAO’s approach reflects a conservative, institutional mindset. Rather than distributing all revenue to token holders, it prioritizes financial stability and reserve accumulation. The trade-off is that MKR holders don’t receive immediate yield—they benefit from long-term protocol strength instead.

Factors Influencing Revenue Distribution

Several variables determine how effectively revenue flows to participants.

Token utility design matters. Tokens that serve multiple purposes—governance, fee payment, collateral, and revenue sharing—tend to maintain stronger value than those with narrow use cases. When a token only offers governance rights, participants may discount its worth since governance often fails to materialize meaningful changes.

Governance quality determines whether revenue actually reaches intended recipients. Well-designed distribution mechanisms can be undermined by incompetent or malicious governance. The best protocols implement time-locks, multi-sig requirements, and proposal thresholds that prevent rash decisions.

Market conditions affect every distribution model. Trading fees plummet during low-activity periods. Staking rewards depend on token price stability. Buyback effectiveness requires sufficient liquidity. Understanding these dependencies helps set realistic yield expectations.

Regulatory uncertainty increasingly influences distribution decisions. Protocols may avoid explicit profit-sharing to prevent securities classification. This has pushed some projects toward contributor rewards or ecosystem grants rather than direct token holder distributions—a nuance often overlooked in DeFi education.

The Honest Reality

After examining dozens of protocols, I must acknowledge something counterintuitive: most DeFi participants actually earn more from token appreciation than from protocol revenue.

Revenue distribution mechanisms often generate modest yields—typically 1-5% annually for stakers on well-established protocols. Meanwhile, early participants in successful protocols have seen far greater returns from token price appreciation. This doesn’t mean revenue distribution is worthless; it means expectations need calibration.

There’s also the matter of information asymmetry. Large token holders with voting power often capture disproportionate revenue shares through governance proposals. Retail participants frequently receive less than they expect after accounting for lock-up periods, gas costs, and dilution from new token emissions.

The space continues evolving rapidly. New models—streamed rewards, perpetual ve systems, NFT-gated distributions—emerge regularly. What remains constant is that understanding distribution mechanics separates informed participants from those chasing yields they never actually receive.

DeFi protocol revenue distribution is a real experiment in economic design. Unlike traditional finance, where profit distribution follows centuries-old legal frameworks, DeFi allows communities to design novel mechanisms and vote them into existence in weeks. The models outlined here will likely change within the next few years as the space matures and competitive pressures intensify.